Source: Abubakar Idris/ Techcabal

Unresolved challenges threaten to limit Nigerian digital payments growth.

Nigerian payments companies fantasize about the death of cash. It’s on everybody’s pitch. We got the first glimpse of this post-cash Nigerian universe in the first and second quarters of 2020 when Covid-19 shut down much of the world’s physical economy triggering an electronic payments boom in many countries, including Nigeria.

While much of society has since adjusted and even returned to normalcy post-pandemic, digital payments have remained. And in countries such as Nigeria, physical cash and digital payments exist side-by-side.

Then in November 2022, the West African country got another glimpse into a world without physical cash. When the Central Bank of Nigeria announced the double whammy of a rushed currency redesign and tighter regulations on mobile money agents, some folks anticipated that the restrictions would push more consumers into the digital payments bubble.

But when the regulator struggled to mint and circulate a decent amount of the redesigned currency before a needless January 31 deadline, it threw the country into a frenzy not seen since the days of the EndSARS protests. Just weeks before the presidential election, the scarcity and the hoarding of cash saw people break into ATMs, go naked in bank halls and cry their hearts out as the nation descended into chaos.

Naturally, electronic payments should have witnessed an impressive uptick, many assumed. But data from Q1 show a different trend.

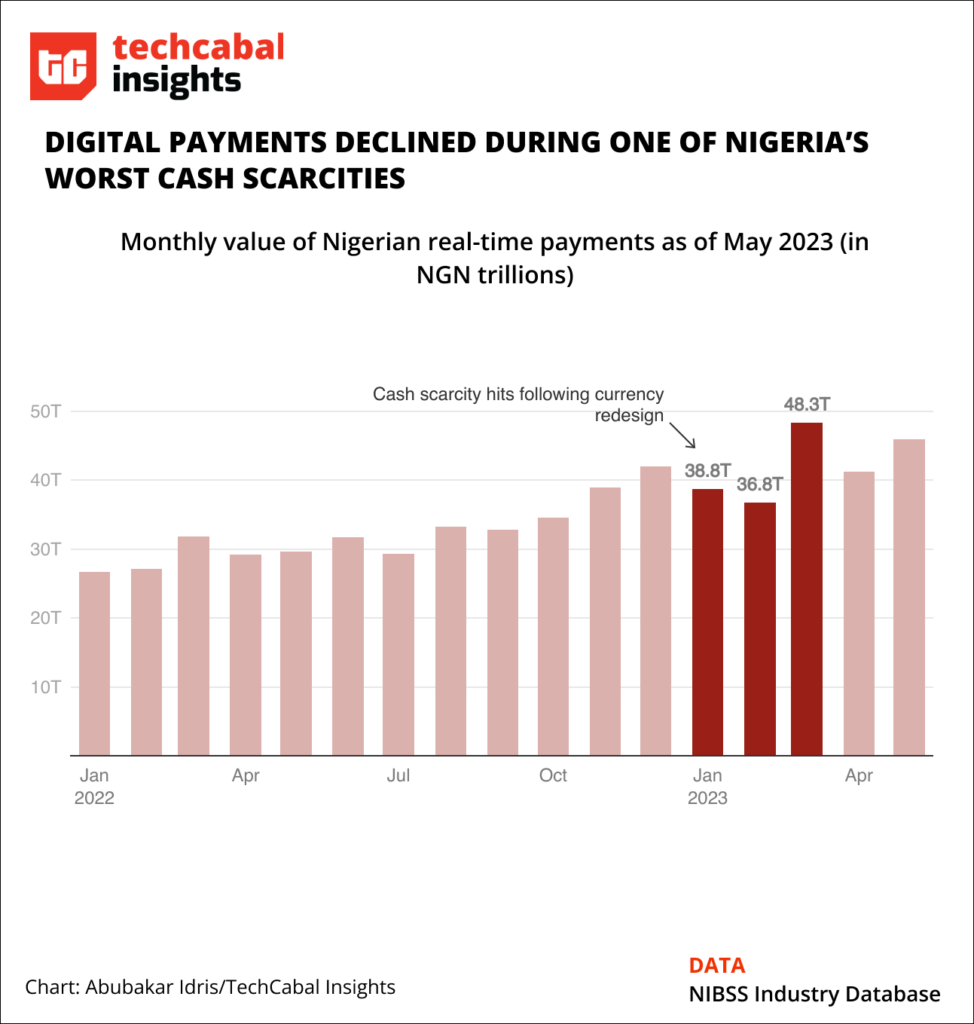

In an economy where a majority of consumer transactions are settled in cash, when an obnoxious cash scarcity hit, instead of a digital payments boom, we witnessed a significant pullback. Within the first two months of the cash scarcity, digital payments in Nigeria plummeted dipping by 7.5% in January, and further declined by 5.12% the next month, according to transaction value data from the Nigerian Inter-Bank Settlement Scheme (NIBSS).

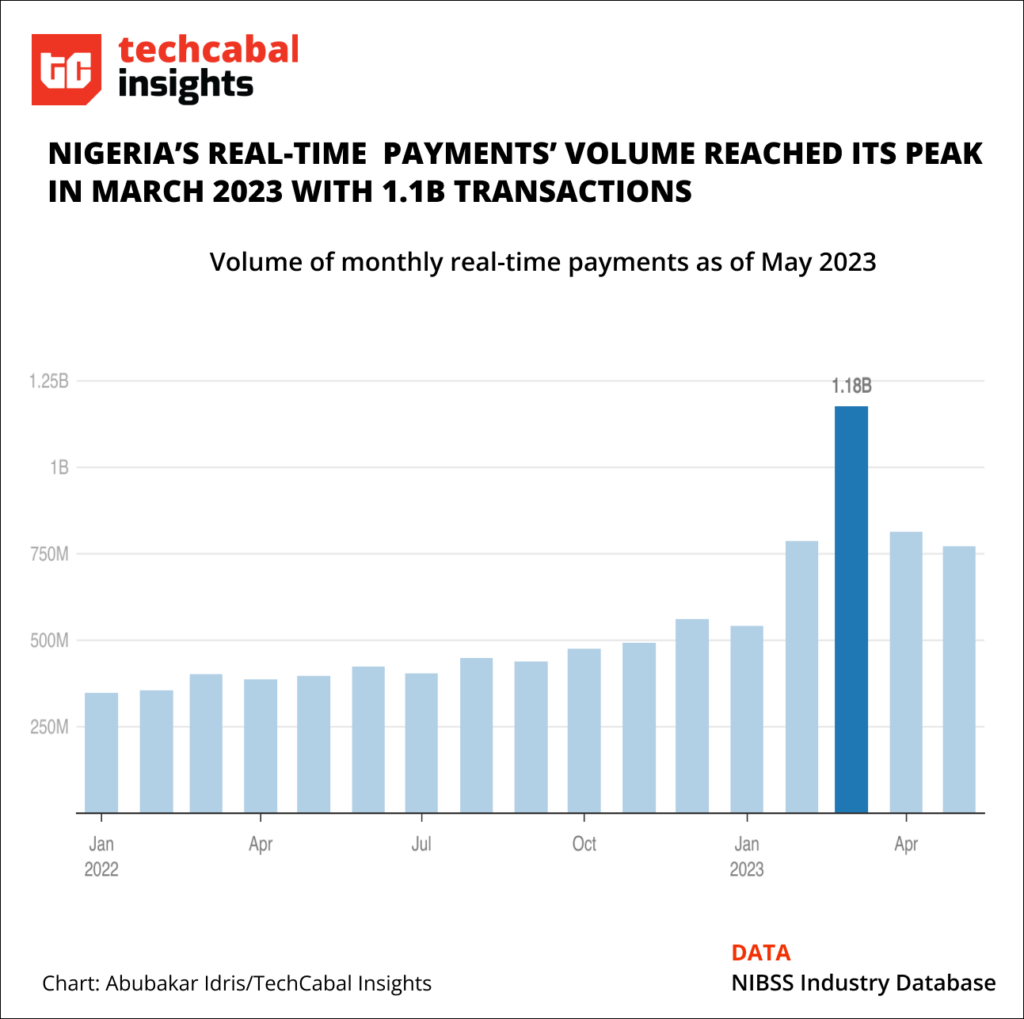

However, the payments value recovered quickly the next month (March) — reaching a record high of ₦48.3 trillion with a transaction volume of 1.18 billion (another record peak) — before plummeting consecutively in April and June.

Interestingly though, while the amount of money Nigerians sent overall declined at the height of the cash scarcity, more people flocked to digital payments during the same period. After recording an initial 3.4% dip in January, payments volume witnessed an uptick till March when the intensity of the cash crunch reduced.

Now, interpreting the data, which is available on the NIBSS Industry Database online, is a little challenging partly because NIBSS hasn’t issued any public statement explaining these payment trends.

On the one hand, historical data suggests the payment declines in early 2023 are not really unusual. Instead, they are fairly consistent with previous years. With its memorable holidays and the influx of fun international travelers, December is the peak month for payments in Nigeria, and each year since 2018, transaction activity tends to surge compared to the trailing eleven months. Equally consistent, transaction values tend to decline in both January and February as Nigerian households adjust to the new year after the holidays. The year 2020 would have been the odd year, but the lockdowns didn’t start until late March 2020. So technically, nothing unusual happened this year.

Yet we know for a fact that Q1 2023 was different, especially with all the progress recorded since 2020. If a large chunk of payments happens in cash, why didn’t the scarcity of the physical naira trigger a bump in digital spending? Why did electronic transactions decline for two straight months despite the ubiquity of payment services? Also worth sharing that out of the five months recorded by NIBSS so far, digital payments reported declines in three.

Again, interpreting the data is not straightforward, but we have a few good guesses.

Macroeconomic realities

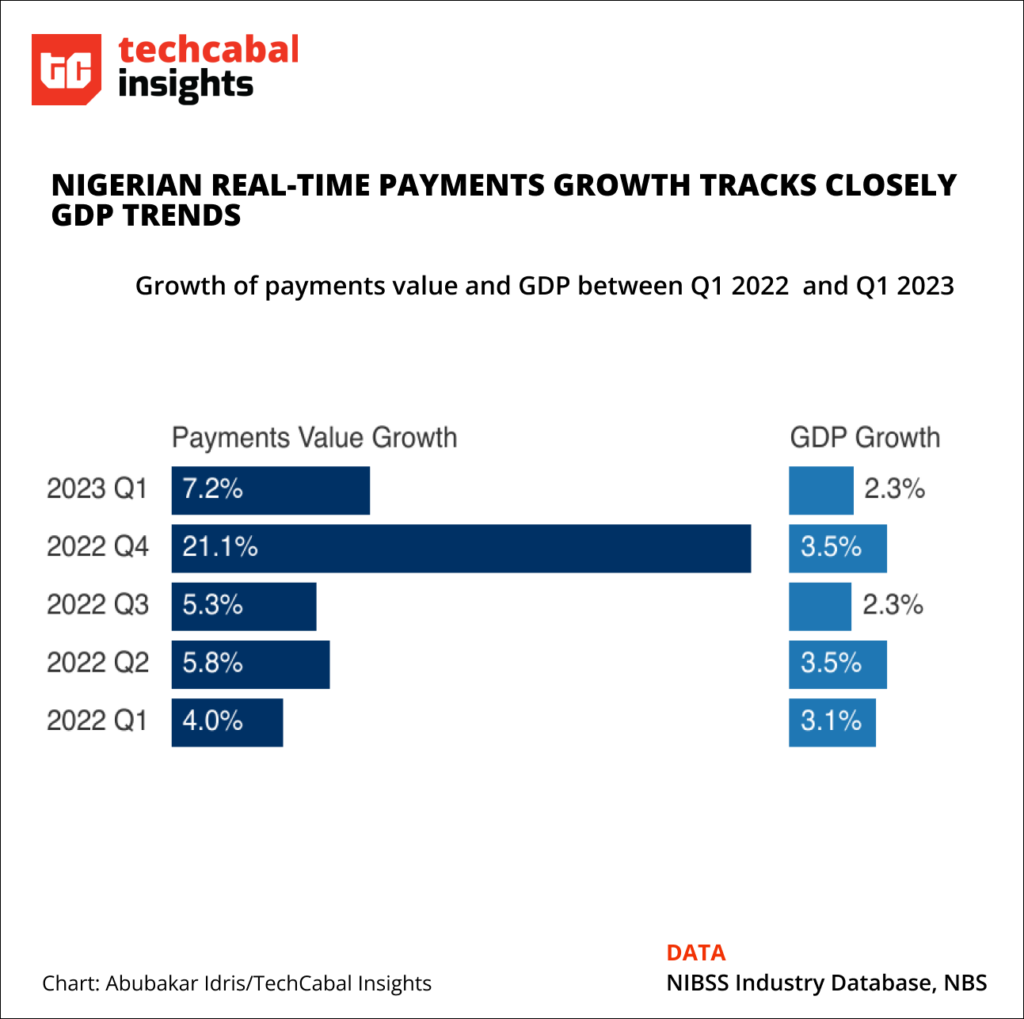

The first answer is economics. After a festive December, Nigerians tend to cut back overall spending in January and February. But the cash scarcity had an outsized impact this time, according to the National Bureau of Statistics (NBS). The economy plummeted at least 3.11% compared to the previous year and the previous quarter.

Yemi Kale, the former head of NBS, predicted the slump, explaining that around 54% of the Nigerian economy is cash-based. In particular, the informal economy, where the average Nigerian works and shops, represents half of GDP, and 90% of transactions are settled in cash.

But economics alone doesn’t answer the question.

Agency banking restrictions and higher mobile agent transfer fees

Ahead of the deadline to switch to the redesigned Naira, the CBN placed restrictions on mobile money agents, effectively blocking agents from carrying out completing larger volumes of payments. But as the cash scarcity hit harder and banks became unreliable for withdrawals, agents took advantage of the situation. They handled more payments, NIBSS data showed, but they also raised prices to incredible proportions in different parts of the country. This trend discouraged people from transacting larger sums. Mobile agency firms are still grappling with how to control the army of 1 million agents loosely under their control.

Digital platform instability

Platform stability was a major focus ahead of the cash scarcity and mobile money restrictions. Everybody anticipated this. The signs were on the wall. In the run-up to the cash crunch, Nigerians reported several network outages by major banks that caused embarrassing transaction failure rates.

It only got worse when cash disappeared from the ATMs. Too many bank apps continued to underperform with weak infrastructure and clunky apps that were unusable for long hours of the day. During the height of the crisis, bank customers complained they were unable to log into some of their fintech apps, while others reported high transaction failure rates.

And as the frustration grew, it exploded with customers breaking down emotionally at banking halls while other folks forced their way into banks, damaging ATMs and other infrastructure.

Startup funding decline

Nigerian startups typically don’t let an opportunity or useful crisis go to waste. During the pandemic, payments companies threw their weight behind e-commerce or online storefronts. When traditional banks goof, say extended transaction downtime, startups are quick to remind people why they exist. When banks restricted international payments with naira cards, fintechs weren’t shy to shoot their shots as virtual dollar card providers. And when BBNaija made a comeback as the biggest show on Nigerian television, tech companies led the way with lucrative sponsorship deals ahead of banks and consumer goods companies. All of these were made possible not just by marketing ingenuitzy, but also the confidence from venture capital funding.

The naira scarcity of January and February came at a stormy period for funding for everybody. With investment outlooks looking bleak, at least for the short term, this was not the time to activate a splashy marketing campaign.

Plus, the incentive to go all out during this period was low. An election period, a macroeconomic pullback, funding concerns, but most importantly, payment fees aren’t high enough to incentivize a sharp deviation from the existing strategies for a crisis that was going to last maybe a week, six months, or a year? It was unclear. And that uncertainty perhaps wasn’t worth it. Companies mostly pushed harder with previous campaigns, including offline efforts, not new ones.

Despite all these challenges, it’s a no-brainer that a couple of companies managed to record some growth in digital payments during one of the most unfortunate periods in recent Nigerian history. Collectively, payments company all hit their peaks in March as awareness of digital alternatives to cash payments grew. But for the months of January and February, when many assumed real-time payments blossomed, it didn’t. The uptick came after. And growth slowed afterward.

Source: Abubakar Idris/ Techcabal